企業向けエネルギーおよび産業用ソフトウェアベンダーの商業構造は、現代の購買行動と機能的に整合していない。 B2Bパイプライン速度フレームワーク, 組織は、このような構造的な不整合を是正し、販売サイクルを短縮し、企業バランスシートに対する体系的な顧客獲得コスト(CAC)の負担を軽減することができる。.

調査によると、現代のエネルギー部門のバイヤーは約 評価過程の61%を匿名で ベンダーと直接連絡を取る前に、独立した調査、ピア検証、技術文書レビューを通じて、この「最初の接触ポイント」(POFC)は、調達委員会がAIファーストの専門ツールを活用して非同期的に候補リストを定義することにより、2024年の69%から2026年には61%に短縮されました。.

ベンダーが重要な製品情報を「デモをリクエスト」という障壁の背後に隠してしまうと、質の高いリードは生まれません。単に購入者の匿名選択プロセスから外れてしまうだけです。8ヶ月の販売サイクルを4ヶ月に短縮するには、ベンダーは B2Bパイプライン速度フレームワーク 購買委員会全体が、営業担当者を介さずに、自己主導で評価を行えるデジタル環境を構築する。.

B2Bパイプライン速度フレームワークは、95:5の資本配分ミスという罠を是正する

産業用ソフトウェアおよびグリッド技術ベンダーは、現在活発な販売サイクルにある市場のごく一部を追いかけるために、顧客獲得予算の最大 90% を誤って配分することで、日常的に「9:1 の評価の罠」を引き起こしています。データは、どの時点でも、, 潜在的なB2Bバイヤーのうち、「市場にいる」のは約5%に過ぎない。“ ソリューションを購入するため。残りの95%のターゲットアカウントは、複数年契約に縛られている、当面の予算がない、または異なる運用サイクルにあるため、「市場外」である。.

このような分布にもかかわらず、B2B マーケターの 96% は、キャンペーンが 2 週間以内にコンバージョン結果をもたらすことを期待しています。この期待により、市場投入 (GTM) チームは、同じ 5% のアクティブ プールをターゲットとした積極的なボトム ファネルのパフォーマンス マーケティング キャンペーンを実行せざるを得なくなります。その結果、GTM 環境は非常に競争が激しくなり、顧客獲得コストは $1,200 という高いベンチマークにまで上昇しました。B2B ソフトウェア企業は現在、マーケティングおよび販売コストに平均 $2.00 を費やして、わずか $1.00 の新規年間経常収益 (ARR) を生み出しています。.

エンタープライズ向けエネルギーソフトウェアの場合、このCACの負担により、投資回収期間は18~24ヶ月に延びます。資本が非効率的で肥大化した8ヶ月のラグタイムに閉じ込められると、企業の評価倍率は機関投資家から大幅な割引を受けます。95%市場外セグメントが購買サイクルに入る前に、リソースをブランド記憶の確立にシフトすることで、企業は長期的なブランドエクイティを構築できます。この戦略的転換を実行することで、 B2Bパイプライン速度フレームワーク 顧客獲得率を逆転させ、販売サイクルを短縮し、受動的な関心を成約済みの収益に2倍の速さで変換することで、高い倍率を実現します。.

技術的なアクセス制限が、最終候補選定戦略を阻害する

現代のGTMの成功には、従来のアウトバウンドセールス手法から、セルフディレクテッドバイヤーイネーブルメントへの移行が必要です。アナリストによると、B2Bバイヤーの61%、特に現在調達委員会を支配しているデジタルネイティブのミレニアル世代とZ世代の専門家は、積極的に “担当者不要の体験 評価の初期段階から中期段階にかけて、彼らは売り込まれることを望んでいません。技術仕様、製品アーキテクチャ図、実例への直接的かつ制限のないアクセスを求めているのです。.

ベンダーがこのドキュメントを制限的なCRMキャプチャの背後に隠蔽すると、摩擦が生じ、購入者が直接競合他社に流れてしまう。調査によると、 81%の購入者は既に優先ベンダーの候補リストを作成済みです。 彼らが最初に営業担当者に連絡した時点で、 95%の受賞候補者リストは初日に決定されます 正式な評価の段階です。販売サイクルへの参入が遅れると非常に不利になるため、ベンダーのウェブサイトは最初のプリセールスエンジニアリングインターフェースとして機能しなければなりません。.

ソフトウェアプロバイダーが存続するためには、最初の販売障壁を取り除き、購買委員会が舞台裏で技術的および運用上の障害を独自に解決できるようにする必要があります。これは、 B2Bパイプライン速度フレームワーク 技術的な支援を拡張しつつ、時期尚早な人的介入を強いることなく、最適化されたアウトバウンド構造を確立する。.

NERC CIP-003-9 サイバーセキュリティ要件が調達における深刻な摩擦を引き起こす

エネルギーおよび公益事業分野では、GTMチームはサイバーセキュリティとサプライチェーンコンプライアンスによって生じる摩擦を過小評価することが多い。2026年4月1日、 北米電力信頼性評議会(NERC) 新たなアップデートが強制適用され、影響の少ない大規模電力系統(BES)のサイバー資産が規制遵守の対象範囲に含まれるようになりました。この拡大により、これまで規制対象外だった分散型エネルギー資源(DER)のうち、推定15%から25%が直接影響を受け、3,300を超える電力会社と独立系発電事業者が規制遵守状況の追跡対象となります。.

下 CIP-003-9 第6項(添付資料1)では、公益事業者は、ベンダーの電子リモートアクセスセキュリティ制御を正式に文書化し、実装する必要があると規定しています。この基準により、ソフトウェアプロバイダー向けの従来のVPN「常時アクセス」は廃止されます。リモートでのメンテナンス、トラブルシューティング、ファームウェアアップデートのセッションはすべて、ID認識プロキシまたはジャンプホストを介して完全に認証され、トラフィックが保護対象資産に到達する前にユーザーレベルで多要素認証(MFA)が行われ、時間制限があり、完全に監視され、完全に記録される必要があります。.

規制リスクに関する警告: NERC CIP 違反には、違反 1 件あたり 1 日あたり 1 TP4T600,000 ~ 1 TP4T200 の厳しい罰金が科せられるため、ベンダーがこれらの基準に即座に監査可能な形で適合していることを証明できない場合、電力会社の購買委員会は調達を即座に凍結します。適合性マッピングは、ベンダーの B2Bパイプライン速度フレームワーク.

二重の重要性評価とCSRD義務化により調達の進捗が凍結される

サイバーセキュリティに加え、サステナビリティ報告規制は、自主的な広報活動から、厳格で法的拘束力のある遵守義務へと移行した。 欧州連合の 企業サステナビリティ報告指令(CSRD)は、EU上場の大企業およびグローバル企業に対し、環境、社会、ガバナンス(ESG)の影響に関する詳細な情報開示を義務付けています。 欧州サステナビリティ報告基準(ESRS), 企業は、包括的なスコープ3温室効果ガス(GHG)排出量を含む、1,000を超える定性的および定量的データポイントについて報告しなければならない。.

EUオムニバスI指令の簡素化パッケージでは、従業員数1,000人以上かつ売上高4億5,000万ユーロ以上の企業に直接適用範囲が限定されているものの、指令のバリューチェーンに関する規定は引き続き有効である。大規模な公益事業者は、バリューチェーンに関する義務を履行するため、サードパーティのソフトウェアおよびハードウェアプロバイダーのESG(環境・社会・ガバナンス)およびカーボンフットプリントを監査する法的義務を負っている。.

つまり、エンタープライズソフトウェアプロバイダーがESRS E1(気候変動)、ESRS E5(資源利用/循環型経済)、ESRS S2(バリューチェーンにおける労働者)にわたる監査可能な指標を提示できない場合、その取引は買い手のコンプライアンス部門で停滞することになります。これらの指標をオンデマンドで積極的に提示することは、産業化された企業の中核的な戦術要素です。 B2Bパイプライン速度フレームワーク.

販売サイクル期間が企業の加重平均資本コストを直接調整する

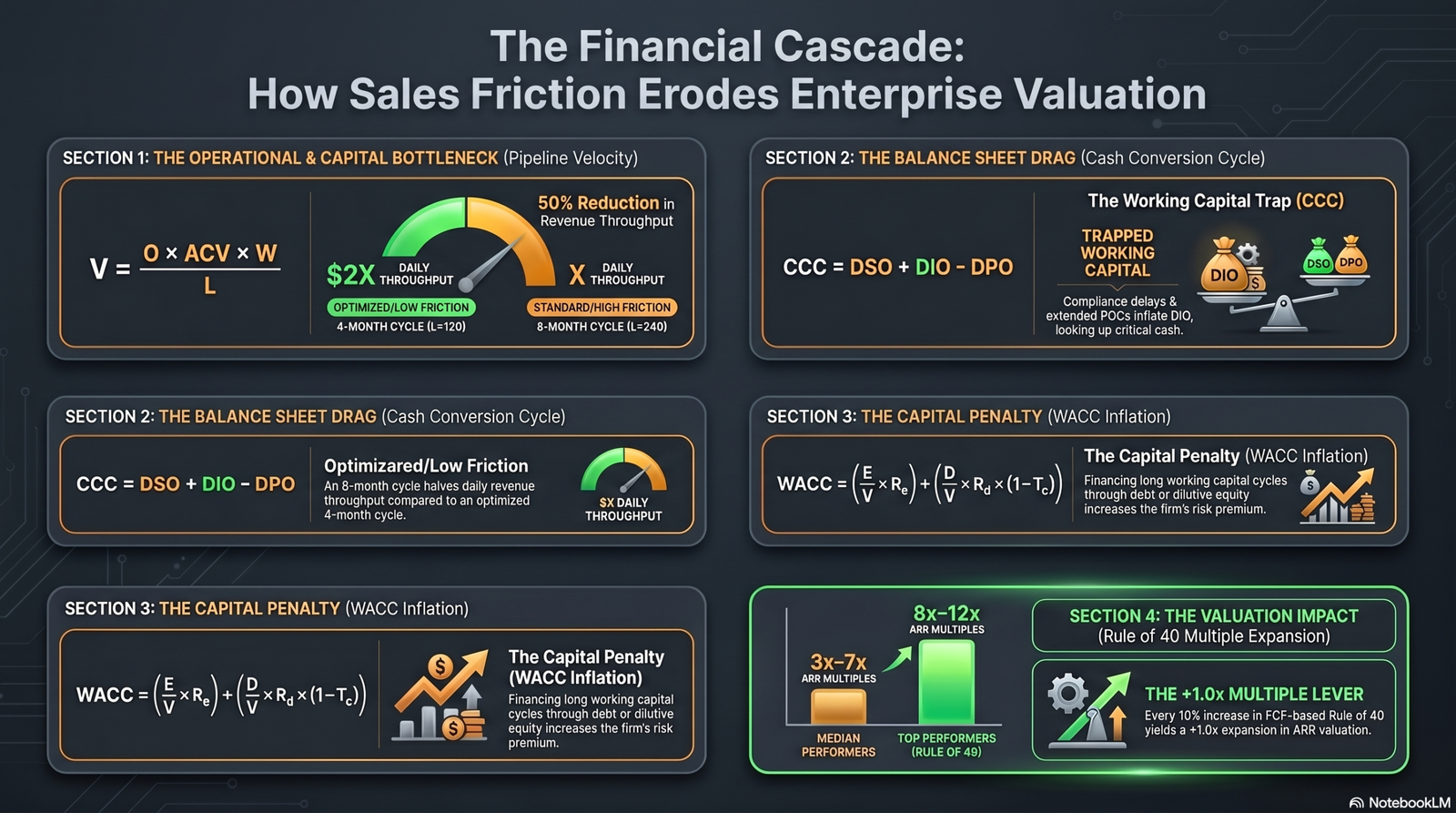

8ヶ月にも及ぶ長期の調達サイクルは、単なる事務的な煩わしさではなく、ベンダーの企業価値を低下させる財政的な負担となる。 B2Bパイプライン速度フレームワーク, この資本の非効率性は、パイプライン速度方程式と、 キャッシュコンバージョンサイクル(CCC), 、そして同社の 加重平均資本コスト(WACC).

B2Bセールスエンジンの1日あたりの収益処理能力は、パイプライン速度の計算式によって定義されます。

$$V=frac{Otimes ACVtimes W}{L}$$

どこ:

-

$V$はパイプライン速度(1日あたりの収益)です。.

-

$O$は、有効な資格のある機会の数です。.

-

$ACV$は、年間平均契約額(平均取引規模)です。.

-

$W$は勝率です。.

-

$L$は販売サイクル期間(日数)です。.

8ヶ月の販売サイクル($L = 240日)は、最適化された4ヶ月サイクル($L = 120日)と比較して、1日の売上高を直接的に半減させます。この遅延は、キャッシュコンバージョンサイクルの在庫日数(DIO)を直接的に増加させます。

$$text{CCC}=text{DSO}+text{DIO}-text{DPO}$$

ソフトウェアおよびハイテクのGTM(Go-to-Market)において、DIO(Daily IO:運転資本期間)は、未請求のプリセールスエンジニアリング、概念実証(POC)統合、およびコンプライアンス検証サイクルに資本が拘束される日数を表します。こうした長期にわたる運転資本サイクルを賄うため、企業はしばしば高コストの負債($D$)または希薄化株式($E$)を調達せざるを得ず、リスクプレミアムと企業の総資本コストが増加します。

WACC = (E/V × R) + (D/V × Rd × (1-Tc))

このバランスシートのマイナス要因は、企業の業績を積極的に低下させる。 40の法則 スコア(収益成長率+利益/FCFマージン)。実証的な評価データによると、非上場のSaaSおよび産業用ソフトウェア企業は、ARRの3倍から7倍の中央値で取引されていますが、40の法則を超えるトップパフォーマーは、ARRの8倍から12倍のプレミアム倍率を誇っています。フリーキャッシュフローに基づく40の法則が10パーセントポイント増加するごとに、企業のEV/収益倍率が約$+1.0x$拡大します(EBITDAベースでは$+0.7x$)。この遅れを克服するには、エンドツーエンドの実装が必要です。 B2Bパイプライン速度フレームワーク これにより、運転資金が解放され、市場投入コストが削減され、企業価値が拡大する。.

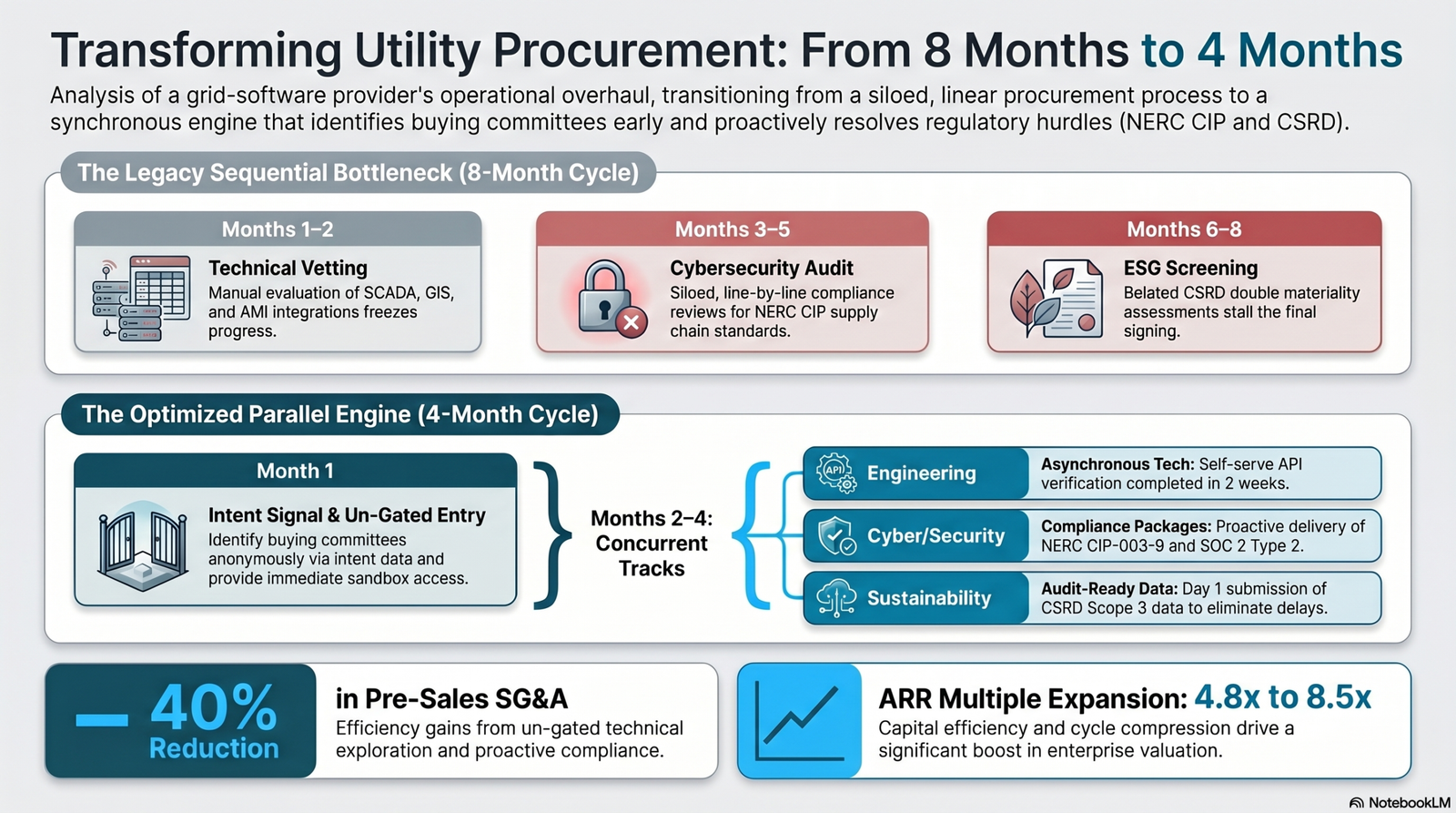

実例分析:スマートグリッドソフトウェアプロバイダーが調達遅延を半減

地域電力系統向けスマート容量計画モジュールの統合に特化した企業向けグリッドソフトウェアプロバイダーは、8ヶ月にも及ぶ煩雑な調達サイクルに常に悩まされていた。電力会社の購買委員会内の複数の部門間で、商業的な摩擦が次々と発生し、結果として高額な販売前エンジニアリング費用とキャッシュコンバージョンサイクルの悪化を招いていた。.

歴史的なボトルネックは、3つの明確な段階に集中していた。

-

1~2ヶ月目(技術審査): エンジニアリング部門は、既存のSCADA、GIS、AMIの統合に関する問題を解決するため、評価を一時停止した。.

-

3~5ヶ月目(サイバーセキュリティ監査): 電力会社のコンプライアンスチームは、NERC CIP-013サプライチェーン評価およびCIP-007-7パッチ評価を手動で実施した。.

-

6~8ヶ月目(ESGスクリーニング): 企業のサステナビリティ部門は、複雑なCSRD(企業の社会的責任開発)の二重重要性評価を手作業で実施していた。.

この問題を解決するために、プロバイダーは完全に以下の3段階のGTMオーバーホールを実施しました。 B2Bパイプライン速度フレームワーク:

1. インテントシグナルアーキテクチャによる匿名委員会識別

従来のようなコールドコールに頼るのではなく、プロバイダーはシグナル駆動型の収益オーケストレーションプラットフォームを導入し、自社および第三者の購買意欲シグナルを追跡しました。匿名のユーティリティアカウントが技術文書ページを繰り返し閲覧したり、特定のコンプライアンスキーワード(例:「CIP-003-9 リモートアクセス」)を検索したりすると、システムは調査の初期段階でそれらを検知しました。これにより、マーケティング部門は、購買委員会の専門家ネットワークが直接連絡を取るずっと前に、カスタマイズされた役立つリソースを直接提供することができました。.

2. 技術的な摩擦の排除(練習不要のサンドボックス)

グリッドソフトウェアプロバイダーは、開発者向けAPI、製品アーキテクチャスキーマ、および統合ガイドラインを完全に公開し、制限的な「デモ依頼」という障壁を取り除きました。また、電力会社のエンジニアが既存のSCADA、GIS、AMIシステムとの統合機能をバックグラウンドで独立してテストできるセルフサービス型の開発者サンドボックスを導入しました。これにより、購買グループは技術調査の大部分を非同期的に完了させることができ、2か月かかっていた逐次的な販売ボトルネックだった技術審査フェーズを、2週間の並行プロセスに短縮することができました。.

3. 調達準備完了ベンダーパッケージ

セキュリティ、法律、財務上の障壁に対処するため、プロバイダーは監査対応済みのコンプライアンス文書を事前にパッケージ化して作成しました。クライアントの調達部門が長文の質問票を送付するのを待つのではなく、プロバイダーは以下のような包括的なパッケージを積極的に提供しました。

-

A SOC 2 タイプ 2 SSAE第18号に基づいて作成された証明報告書。.

-

CIP-003-9、CIP-013-1、およびCIP-007-7との整合性を証明する、事前にコンパイルされたNERC CIP準拠ガイド。.

-

CSRDに準拠したサステナビリティ開示情報。これには、検証済みのスコープ3温室効果ガス排出量データや、ESRSテンプレートに直接マッピングされたサプライチェーン労働基準評価などが含まれます。.

この積極的なコンプライアンスパッケージにより、電力会社の法務、コンプライアンス、およびサステナビリティチームは、技術評価と並行してベンダーの監査を実施することができた。.

この戦略の運用上の成果は即座に現れ、非常に測定可能でした。平均販売サイクルを8ヶ月から4ヶ月に短縮することで、 B2Bパイプライン速度フレームワーク, プロバイダーは、販売前のSG&Aコストを40%削減しました。パイプラインカバレッジ比率は健全な$4text{x}$ベンチマークに正常化し、予測リスクを排除しました。この資本効率と成長率の改善により、同社の暗黙のARR倍率は$4.8text{x}$から$8.5text{x}$に拡大し、次回の資金調達ラウンド前に大きな企業価値を解放しました。.

戦略的要点:GTMリソースの即時再配分が必須

-

61%匿名旅は譲れない。 現代のB2Bエネルギー購入者は、評価プロセスの61%を独自調査によって完了させています。デモ依頼の背後に技術仕様を制限として設けることで、価値の高い見込み客は制限のない競合他社を選択せざるを得なくなります。.

-

9:1の罠は資本効率を損なう: 90%の買収予算を5%の市場内セグメントに誤って配分すると、CACが持続不可能な高さまで上昇し、企業価値が低下します。自動化された B2Bパイプライン速度フレームワーク 商業資本を保護する。.

-

規制の抜け穴が即座に氷取引を成立させる: NERC CIP-003-9の厳格なベンダーリモートアクセス基準とCSRDスコープ3の炭素排出量報告義務は、監査対応可能なコンプライアンスエンジンを通じて積極的に対処しない限り、調達を停滞させる。.

-

販売速度が複数倍の事業拡大を促進する: 販売サイクルを8ヶ月から4ヶ月に短縮することで、パイプラインの1日あたりの売上高が2倍になり、顧客獲得コスト(CAC)の回収期間が短縮され、プライベート顧客における収益倍率がプレミアムな年間経常収益(ARR)の8倍~12倍の水準にまで拡大します。.

重要な規制および財務に関する調査には、標準化された解決策が必要である。

B2Bパイプライン速度フレームワークがEBITDAマージンに及ぼす直接的な影響

ベンダーは、技術文書の公開制限を解除し、セルフサービス型のサンドボックスを導入することで、購買委員会が最大70%の技術調査を非同期的に完了できるようにします。これにより、初期および中期のファネル段階における、頻繁かつ手作業によるプリセールスエンジニアリングの介入の必要性が軽減されます。さらに、販売サイクルの加速により、顧客獲得コスト(CAC)の回収期間が18~24ヶ月から12ヶ月未満に短縮され、販売費および一般管理費(SG&A)が削減され、EBITDAマージンが拡大します。.

NERC CIP-003-9におけるGTMオペレーションに影響を与える主要な規制トリガー

NERC CIP-003-9 に基づき、低影響のバルク電力システム (BES) サイバーシステムは、文書化されたベンダーの電子リモートアクセスセキュリティ制御を実装する必要があります。ベンダーは共有 VPN アカウントに依存することはできなくなり、すべてのセッションはユーザー識別、MFA 認証、時間制限、および記録が必要です。ベンダーが安全なジャンプホスト統合またはセッション無効化機能の証明を提供できない場合、電力会社の調達チームは、そのベンダーを候補リストに含めることが法的に禁止されます。 B2Bパイプライン速度フレームワーク コンプライアンス関連文書を初日から利用できるようにすることで、この摩擦を回避します。.

CSRD義務に基づく電力購入者向けスコープ3排出量の定量化

SaaSおよびソフトウェアベンダーは、GHGプロトコルに従い、上流および下流の活動全体にわたる企業のカーボンフットプリントを計算し、開示する必要があります。これには、直接的な運用排出量、データホスティングのエネルギー使用量、サプライチェーンへの影響が含まれます。CSRD ESRS E1規格では、大手バイヤーは、独自のバリューチェーンのサステナビリティ開示を作成するためにこれらの指標を必要とします。事前にコンパイルされ、監査済みのESGデータパッケージを提供することで、調達における大きな遅延を回避できます。.

著者について:

について プロジェクト54 チーム は、エネルギー、産業技術、エンタープライズSaaS分野における商業効率の向上に重点を置く、B2B市場アナリストとGTM戦略立案者からなる専門グループです。.