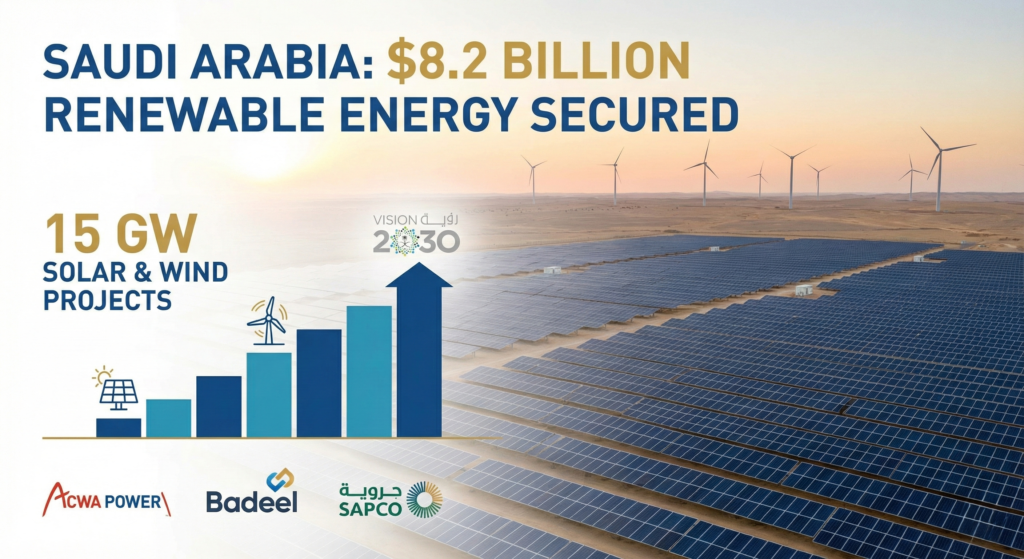

沙特阿拉伯已成功为七个大型太阳能和风能项目组成的标志性项目组合实现了融资交割,向王国电网改造注入了$82亿。这项于2025年12月2日宣布的交易,降低了该国在“沙特绿色倡议”和“2030愿景”下雄心勃勃的清洁能源转型计划的重大风险。.

这个巨大的 资本支出 部署,由沙特阿美电力公司(SAPCO)、ACWA Power 和水与电力控股公司(Badeel)等国家冠军组成的联盟牵头,证实王国正积极从宏伟目标迈向硬性基础设施。这七个项目,总计12吉瓦的太阳能和3吉瓦的风能,预计将在2027年下半年至2028年上半年全面投入运营。.

策略、供应和融资动态

这项交易是 政策 愿景2030中制定的承诺,其目标是到2030年实现58.7吉瓦的可再生能源装机容量。这一推动由两大主要因素驱动:

- 腾出石油用于出口: 通过利用低成本的国内可再生能源满足因制冷和海水淡化需求激增而飙升的当地电力需求,沙特阿拉伯最大化了高价值原油的出口量,从而提高了国家收入。.

- 全球脱碳领导力 发展是沙特阿拉伯实现2060年净零排放目标的关键。.

融资结构本身就开创了新的先例 融资 中东和北非地区的大型项目。公共投资基金(PIF)通过其子公司发挥了核心作用,这凸显了主权承诺,从而大大降低了国际贷方和投资者的感知风险。.

BD领袖的有利情景

15吉瓦的财务承诺为整个项目生命周期创造了即时的、切实的机会。.

甲、电网和输电投资

整合 15 吉瓦的间歇性能源需要对现有电网进行大规模升级。这笔交易预示着高压直流输电(HVDC)、先进电池储能系统(BESS)和数字智能电网管理技术将陆续进行招标。专注于电力市场稳定和输电基础设施的公司现在将在该王国迎来多年的繁荣期。.

二、制造业和服务业的本地化

沙特阿拉伯工业发展基金(SIDF)及其国内价值(ICV)计划与这些大型项目紧密相连。其规模之大 需求 太阳能光伏组件、风力涡轮机部件和支架系统的钢材,为建立本地或区域制造基地提供了强有力的商业案例。例如,在更广泛的领域中,我们看到了本地化的主要先例 碳氢化合物 该领域,全球钻井和油田服务公司长期以来一直与当地企业合作,以满足沙特阿美的 ICV 要求。这一模式现在正直接应用于绿色经济。.

三、氢能与水能的关联

廉价、大规模可再生能源的开发直接促成了该王国雄心勃勃的绿色氢能和氨项目,例如旗舰项目 NEOM。这家 15 吉瓦的工厂不仅将为国内电网供电,还将可能为未来的工业脱碳计划提供支持,包括为大型反渗透海水淡化厂供电,直接解决水-能源关联问题。通过确保低成本电力 供应, 绿色商品出口的商业可行性得到加强。.

风险与缓解先例

尽管融资已完成,但高管们必须注意执行风险。.

- 供应链通胀 光伏组件和专业建筑劳务的全球市场依然紧张。沙特项目的规模可能会推高区域价格。审慎的策略包括现在就与一线供应商签订长期主供应协议 (MSA)。.

- 才能与能力 在2027/2028年的紧迫时间表中交付15吉瓦的工程量将给当地的工程、采购和施工(EPC)能力带来压力。项目开发商必须战略性地利用全球EPC专业知识,同时整合当地分包商以遵守本土化内容(ICV)的要求。这种平衡至关重要,关系到能否按时交付。.

- 提货确定性 沙特电力采购公司 (SPPC) 将全额购买产能。这种政府支持的购电协议 (PPA) 结构提供了稳健的收入确定性,这是吸引国际投资的关键降险要素。 融资. 阿联酋阿尔达夫拉太阳能光伏项目的国家支持购电协议先例,展示了这些协议的高度安全性。.

82 亿美元的$财务交割并非终点,而是中东和北非地区有史以来最大规模能源基础设施建设的起点。为了抓住这个为期数年的机遇,战略重点必须转向卓越执行、供应链韧性和最大化国家价值。.

对于在该地区开展业务的能源管理人员来说,这场对峙不仅仅是一场外交争吵,它还严重破坏了 供应/需求 北非的平衡,以及地缘政治风险正在对区域基础设施资产重新定价的信号。.

背景:相互依存的陷阱

该交易旨在同时解决两个问题。以色列天然气过剩,出口路线有限(没有自己的液化天然气设施)。埃及天然气短缺,国内电力需求激增,而伊德库(Idku)和达米特(Damietta)的液化天然气出口能力闲置。.

- 计划 雪佛龙公司及其合作伙伴承诺投入巨资,扩大利维坦的生产,并建造一条新的海上管道(尼察纳航线),以绕过现有的基础设施瓶颈。.

- 现实 以色列总理内塔尼亚胡于 2025 年底暂停了审批程序,将天然气交易与有关加沙边境和西奈半岛的更广泛安全谈判联系起来。.

分子流的这种政治化打破了 “商业盾牌”,在过去五年中,这种盾牌在很大程度上保护了以色列-埃及天然气贸易免受政治动荡的影响。.

风险:资本支出、交易对手和可信度

投资者的信心是这一暂停的直接受害者。.

- 搁浅资本支出潜力:

利维坦项目 1B 和 2 期的扩建需要价值数十亿美元的最终投资决策(FID)。这些最终投资决策以确定的承购协议为前提。如果埃及的承购协议不确定,合作伙伴(雪佛龙、NewMed、Ratio)就无法启动上游资本支出。11 月 30 日 “这一最后期限对于这些决定来说是一个关键的关口;如果过了这一期限而问题仍未解决,整个项目的时间表都将岌岌可危。.

- 埃及的能源脆弱性:

埃及已经在努力解决电力短缺问题。政府已将以色列的这些增量计入其 2026-2030 年发电战略。如果这些天然气不能运抵,埃及将面临两个昂贵的选择:

- 增加对燃油发电的依赖(排放更高、成本更高)。.

- 从全球现货市场进口更多液化天然气,消耗外汇储备。.

- 液化天然气再出口模式:

埃及通过将以色列天然气作为液化天然气再出口到欧洲来赚取硬通货的战略实际上已经暂停。这使开罗失去了偿还主权债务和稳定货币所需的重要收入来源。.

上行情景和战略支点

这笔交易已经破裂了吗?很可能没有。对双方来说,经济逻辑仍然是压倒性的。.

- 大交易 “方案: 历史表明,能源往往成为更大规模外交交易的甜头。如果安全争端得到解决,天然气交易将作为更广泛的正常化方案的一部分获得批准。如果安全争端得到解决,该项目就能快速推进,合作双方可能会优先考虑新管道,以挽回失去的时间。.

- 替代路线: 这种摩擦可能会加速以色列对其他出口路线的探索,例如讨论已久的通往土耳其的管道或浮式液化天然气(FLNG)设施。对于 BD 公司的高管来说,这开辟了新的潜在合作渠道:如果埃及路线被认为政治风险过高,那么技术提供商就可以为以色列提供技术。 液化天然气 以色列运营商可能会对该项目重新产生兴趣。.

行政外卖

利维坦扩张计划的瘫痪可以作为一个案例研究,说明 政治风险管理. .对于投资中东和北非跨境基础设施的公司来说,教训是显而易见的:商业可行性是必要的,但还不够。合同必须包括对政治不可抗力的有力缓冲,供应组合必须多样化。在政治阀门重新打开之前,东地中海仍然是一个高基准的能源市场。.