The Corporate sustainability Reporting Directive (CSRD) effectively criminalizes vague energy marketing by tethering brand narratives to audited, machine-readable financial data.

The Corporate Sustainability Reporting Directive (CSRD) represents a seismic shift from discretionary “green” marketing to a regime of forensic, audit-grade accountability for the energy sector. By tethering brand narratives to machine-readable financial data and mandatory European Sustainability Reporting Standards (ESRS) standards, the directive effectively criminalizes vague environmental claims and exposes “transition-washing” as a high-stakes legal liability. For executives, survival in this new “Age of Accountability” requires reconciling public Net Zero pledges with audited reality, moving away from siloed PR narratives toward a “connectivity” model where sustainability data is legally equivalent to financial performance.

The Sector Risk Scorecard

In the sweeping history of global energy, we have seen maps redrawn by the steam engine, the oil derrick, and the silicon chip. Today, a new map is being drafted, not in the oil fields of the Permian but in the regulatory chambers of Brussels. The CSRD is not a reporting exercise; it is the “Age of Accountability.”

For decades, the energy industry treated “sustainability” as a narrative exercise, a collection of glossy PDFs and aspirational slogans. That era has ended. We are entering a forensic age where the “Transparency Paradox” defines the challenge: the more an organization is required to disclose, the less room it has to hide.

Table 1: Risk Scorecard: EU Energy Sector (2024–2028)

|

Risk Category |

Severity |

Regulatory Driver |

Sector Impact |

|

Legal Exposure |

High |

EU Green Claims Directive |

Fines up to 4% of annual turnover for “unsubstantiated” marketing. |

|

Financial Impact |

High |

ESRS E1-9 (Lock-in Effect) |

Asset devaluations if portfolios conflict with IEA Net Zero scenarios. |

|

Data Integrity |

Critical |

XHTML/iXBRL Mandate |

Real-time algorithmic benchmarking by institutional investors. |

|

Market Access |

Medium |

EU Methane Regulation |

Potential exclusion from EU gas markets for non-reconciled imports. |

The Shift to Mandatory Forensic Accounting

The transition from legacy frameworks (GRI/TCFD) to the CSRD architecture represents a move from “choose your own adventure” reporting to a rigid, regulated science.

Table 2: Evolution of Energy Reporting Standards

|

Feature |

Voluntary Era (GRI / TCFD) |

Mandatory Era (CSRD / ESRS) |

|

Legal Status |

Market-led / Discretionary |

Legally Binding |

|

Materiality |

Single (Financial) Focus |

Double Materiality (Impact & Financial) |

|

Assurance |

Often unaudited |

Mandatory Third-Party Audit |

|

Format |

Narrative PDF / Website |

Machine-readable XHTML |

|

Scope 3 Data |

Discretionary / Estimates |

Forensically Audited (Category 11 Focus) |

|

Enforcement |

Reputational risk only |

Civil and Criminal Liability |

The Data-Narrative Collision: Mapping the Greenwashing Trap

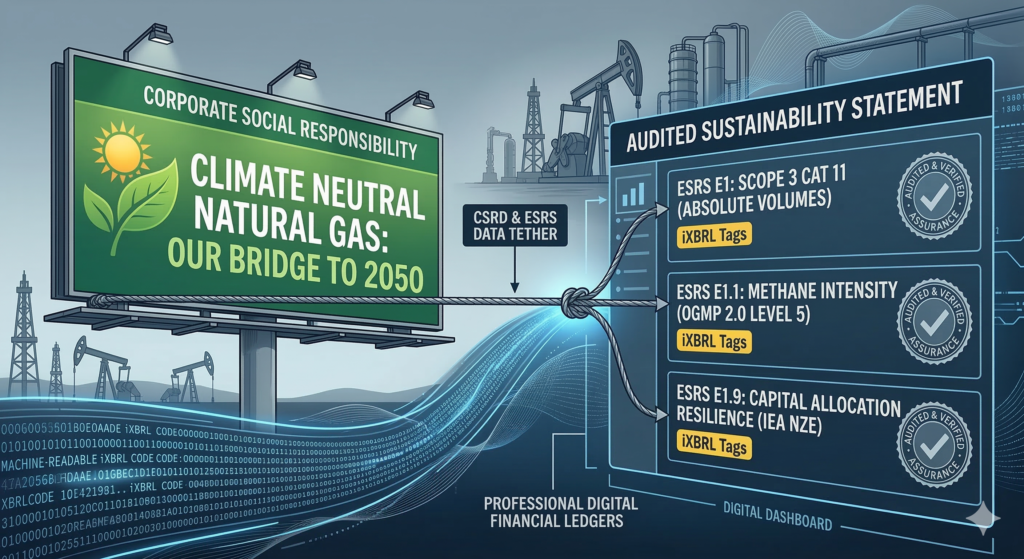

A structural fracture has appeared between the marketing department and the compliance office. Under the EU Green Claims Directive, independent verifiers must validate environmental claims before publication. If a brand promotes a “Bridge to the Future” while its audited The European Sustainability Reporting Standards (ESRS) E1 data shows rising methane intensity, that brand creates an immediate legal liability.

Table 3: Marketing Conflict Matrix

|

Common Marketing Narrative |

CSRD Disclosure Reality (Conflict) |

Legal/Reputational Consequence |

|

“Natural Gas as a Bridge Fuel” |

Absolute Scope 3 Methane intensity (ESRS E1) |

Litigation from NGOs using audited industrial data. |

|

“Climate Neutral LNG” |

Scope 3 Category 11 high-intensity disclosure |

Advertising stop-orders under Green Claims Directive. |

|

“Leading the Transition” |

Capex primarily allocated to fossil exploration |

ESG rating downgrades by MSCI and Sustainalytics. |

|

“Eco-friendly Infrastructure” |

Proximity to biodiversity-sensitive zones |

Violation of ESRS E4; forced ad withdrawals. |

ESRS Deep-Dive: Climate, Pollution, and the “Lock-in” Effect

The strategic center of gravity lies in ESRS E1 (Climate Change). For oil and gas majors, (Scope 3 Category 11) the emissions from the products they sell represents approximately 80% of their total impact. CSRD mandates the disclosure of these absolute volumes, removing the ability to “offset” narratives with peripheral renewable projects.

Carbon Lock-in & Stranded Assets: ESRS E1-9 requires executives to disclose the financial resilience of their strategy against climate scenarios. If a company markets long-term growth while investing in frontier projects that require $60/bbl oil, and the IEA World Energy Outlook projects a price of $25/bbl in its Net Zero Scenario (NZE), that company is now legally obligated to disclose these assets as “locked-in” or potentially stranded. ESRS E2 (Pollution) further demands granular reporting on Nitrogen Oxides and Sulfur Oxides, stripping away the ambiguity from “clean gas” narratives.

Methane Rigor: Contrast of OGMP 2.0 vs. EU Regulation

Methane is the invisible challenge of the gas industry. The 2024 EU Methane Regulation has adopted the Oil & Gas Methane Partnership (OGMP 2.0) as its yardstick. The era of “desktop estimates” is over.

Table 4: Methane Measurement Maturity Levels

|

OGMP 2.0 Level |

Technical Requirement |

Strategic Value |

|

Levels 1–3 |

Generic factors / Desk estimates |

Compliance minimum; carries high investor skepticism. |

|

Level 4 |

Direct source-level measurement |

Identifies specific leak points for immediate repair. |

|

Level 5 (Gold) |

Reconciled bottom-up & top-down data |

Mandatory for future EU regulatory equivalency. |

Case Studies: The Great Divide in “Connectivity”

“Connectivity” is the legally mandated integration of sustainability data into the Management Report in XHTML format. It ends the “sustainability silo.”

- Enel & Iberdrola (The Pioneers): These European utilities have mastered “Integrated Reporting.” Iberdrola uses “leaf symbols” within its financial statements to show exactly how a green investment drives a specific financial outcome. Their data is “connected.”

- The US Supermajors (The Friction): As entities like Exxon or Chevron navigate the EU market, they face “decoupling.” Their public messaging remains focused on traditional energy security, creating a friction point with European regulators who demand a direct, audited link between decarbonization claims and capital allocation.

The Anti-Greenwashing Playbook: The Audit-Safe Lexicon

For the Chief Sustainability Marketing Officer, the vocabulary of the past is now high-risk. Teams must replace the language of “aspiration” with the language of “verification.”

Table 5: The Audit-Safe Lexicon for CSMOs

|

High-Risk Marketing Phrasing |

Low-Risk “Safe-Harbor” Alternative |

|

“Climate Neutral Natural Gas” |

“Gas with 0.15% methane intensity, verified via OGMP 2.0 Level 5.” |

|

“Committed to a Green Future” |

“Investing €X billion in EU Taxonomy-aligned capacity by 2030.” |

|

“Our Energy is Eco-friendly” |

“75% of our portfolio is taxonomy-aligned and audited under CSRD.” |

|

“Sustainable Aviation Fuel” |

“Biofuel with 70% life-cycle GHG reduction (Methodology: PEF).” |

Project 54 Perspective:

In this forensic world, your website is no longer just a brochure for humans; it is a database for machines. Project 54 implements a “Triple-Threat” strategy to ensure your data is indexed correctly by AI.

- AEO (Answer Engine Optimization): We use “Snippet Bait”, meaning direct, factual answers under high-intent headings, to ensure Perplexity and Gemini cite your brand as the primary authority.

- GEO (Generative Engine Optimization): We leverage High-Density Data Tables to provide “Information Gain.” AI models prioritize sources offering structured data over pure text.

- Entity Clarity: We link your brand entity to proprietary concepts, such as the Jantelös™ Method, training AI to associate your organization with high-level strategic thought.

FAQ: Strategic Insights for Snippet-Ready Visibility

How does CSRD impact Scope 3 reporting for Oil and Gas?

CSRD mandates the disclosure of absolute Scope 3 Category 11 emissions in an audited, machine-readable format. This removes the ability to rely on discretionary estimates and forces a direct comparison between marketing claims and actual industrial output.

What is the “Carbon Lock-in” risk in energy B2B lead generation?

Carbon Lock-in refers to infrastructure incompatible with 1.5℃ pathways. B2B buyers now seek “Decision Enablement” content that proves an investment will not become a stranded asset as oil prices potentially drop toward the IEA’s $25/bbl scenario.

How do energy brands ensure visibility in ChatGPT and Claude?

Brands must provide structured, pre-validated data using XHTML-ready structures. By placing “Key Takeaway” boxes and outcome-focused headers at the top of content, brands increase the probability of being cited verbatim by AI models.

Source Citations

- EFRAG Delegated Acts (ESRS): The Regulatory Foundation

- IEA World Energy Outlook 2025/2026: Price & Transition Scenarios

- EU Green Claims Directive: Verification Mandates

- OGMP 2.0 Framework: Methane Gold Standard